An investment decision is only as sound as the information on which it is based. Financial projections, market analysis, and management presentations provide one dimension of that picture. Legal due diligence provides another — and it is the dimension that most directly determines whether the investment is structured on solid ground, whether the assets being acquired are unencumbered, and whether the counterparty is who they represent themselves to be.

Legal due diligence is not a box-ticking formality to be completed after a deal has been agreed in principle. It is a substantive investigative process that shapes how a deal is structured, what protections are built into the transaction documents, and sometimes whether the transaction proceeds at all.

What Legal Due Diligence Covers

The scope of legal due diligence varies depending on the nature of the investment, but typically encompasses several core areas:

- Corporate structure and ownership — Confirming the legal existence of the entity, its ownership structure, any restrictions on transfer of shares or interests, and the authority of those executing documents on behalf of the company.

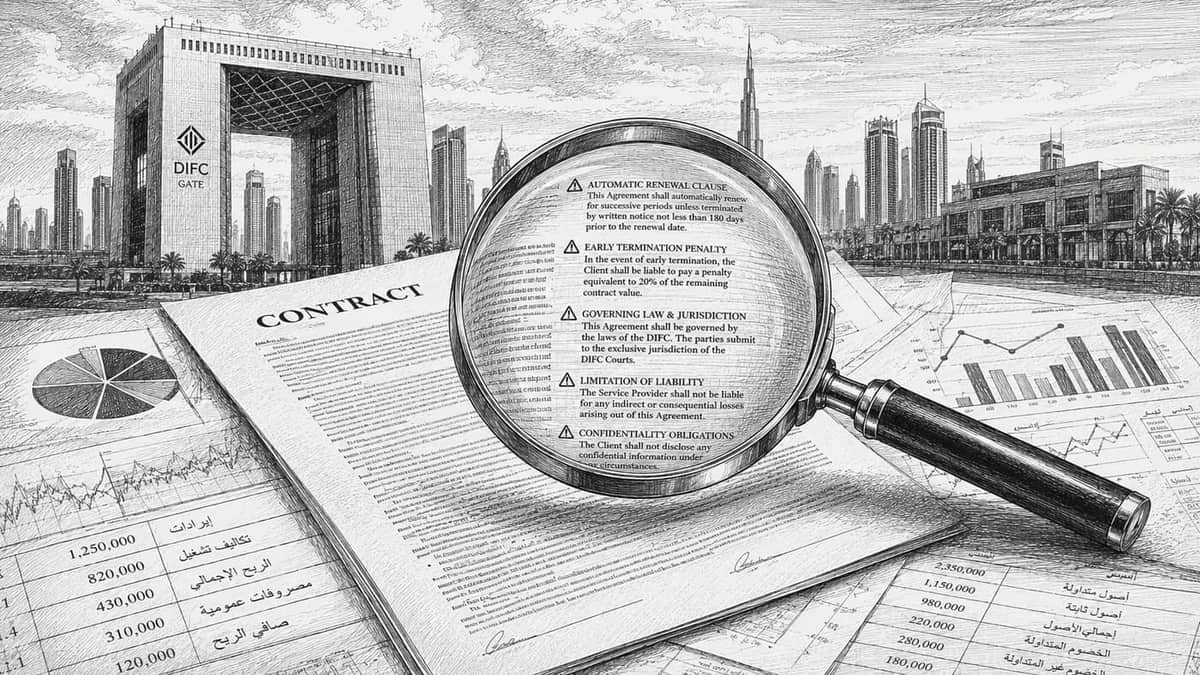

- Material contracts — Reviewing the key commercial agreements the target is party to, including customer contracts, supplier agreements, joint ventures, and licences, to identify onerous terms, change-of-control clauses, or provisions that may be affected by the transaction.

- Regulatory status and licences — Verifying that the business holds the necessary licences and approvals to operate lawfully, and that there are no regulatory investigations, enforcement actions, or compliance gaps.

- Litigation and disputes — Identifying any pending or threatened legal proceedings that could represent contingent liabilities, and assessing the likely outcome and financial exposure.

- Intellectual property — Confirming ownership and registration of key IP assets, identifying any third-party claims or licencing arrangements that could affect the value or use of those assets.

- Employment matters — Reviewing employment contracts, termination liabilities, and any outstanding employee claims, particularly in the UAE where labour law imposes specific obligations on employers.

Due diligence does not create problems. It reveals them — while there is still time to address them.

Counterparty Investigation

In the UAE's international business environment, where counterparties frequently operate across multiple jurisdictions through complex corporate structures, background investigation forms an important part of the due diligence process. Understanding who the ultimate beneficial owners of a business are, whether they have a history of litigation or regulatory action, and whether the corporate structure reflects the commercial reality represented to investors are not peripheral questions. They go directly to the credibility of the investment thesis.

KYC and AML compliance requirements in the UAE have strengthened considerably in recent years, and the consequences of failing to conduct adequate counterparty investigations extend beyond commercial risk to regulatory exposure for the investor.

The Contract as the Investment Itself

Once due diligence is complete, its findings must be reflected in the transaction documents. Representations and warranties, indemnities, conditions precedent, and price adjustment mechanisms are the legal tools through which the risk allocation revealed by due diligence is translated into contractual protection. A strong due diligence process that is not followed by appropriately drafted transaction documents provides incomplete protection.

Conversely, well-drafted transaction documents that are based on inadequate due diligence may provide theoretical protection that cannot be practically enforced — because the problem was not identified clearly enough to be specifically addressed.

When Due Diligence Reveals Problems

It is worth addressing directly what happens when due diligence reveals material issues. This is not the exception — it is a frequent outcome, particularly in complex transactions. The options available include renegotiating the price to reflect identified risks, requiring remediation of specific issues before closing, obtaining specific indemnities to cover identified liabilities, or in some cases concluding that the risk profile of the investment is incompatible with the investor's objectives.

All of these outcomes are preferable to discovering the same problems after closing, when the leverage to address them has been substantially reduced. The cost of thorough due diligence is modest relative to the investments it informs — and relative to the cost of undiscovered problems that materialise after commitment.